Monthly Market Update

Monthly Market Update

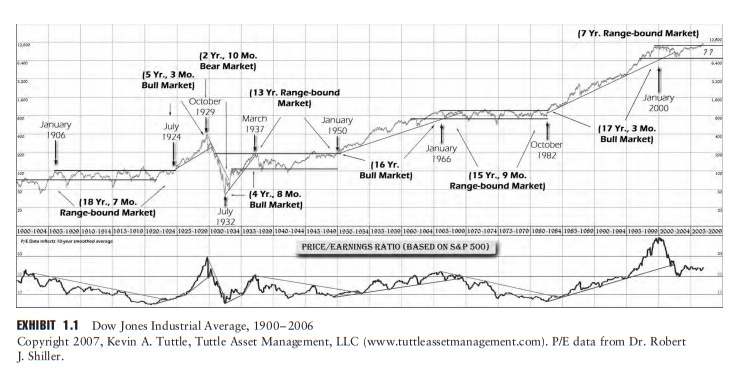

Don't be afraid of a Range Bound Sideways Market

After quite a volatile first six months, the BSE 500 Index rose 10.99% in July to return to where it was at the start of the year.

This sideways market trend is likely to continue because of concerns about stagflation, which might result from central banks around the world raising rates too aggressively to fight inflation.

A range-bound sideways market, which investors and very afraid of at the moment, is quite common if you look at the data from the past century of the US stock market. Out of the 100 years, the US stock market was in a range-bound sideways market for 46 years and still, in the end, managed to return a 9% compound annual return to the investor.

The truth is that no correlation has been found between Stock Market Returns and a Country’s GDP growth over any significant period of time. The market always overreacts to Macroeconomic data in the short term. It never realizes that the data to which it responds, like inflation rate, unemployment number, and retail sales, continuously get revised in the following months to a more accurate figure.

The short-term rise in the stock market in July was because Jay Powell of the US Fed hinted that the aggressive interest increases by the fed would have to slow down sooner rather than later. Now the markets are pricing in an interest rate drop at the start of 2023.

Future events have always resulted in a large number of such forecast’s being plain wrong. Making forecasts about the future levels of the market is much more in the realm of abnormal psychology than financial analysis.

Future Outlook

I hate to be the one delivering the bad news, but the current valuations of companies are still relatively high, and a market correction is still due. Even though no one can predict how long the market will remain irrational, I can confidently say that valuations always revert back to the mean sooner or later, and right now, I think we are closer to the former.

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system and it is not functioning properly”.

—Jeremy Grantham, Barron’s

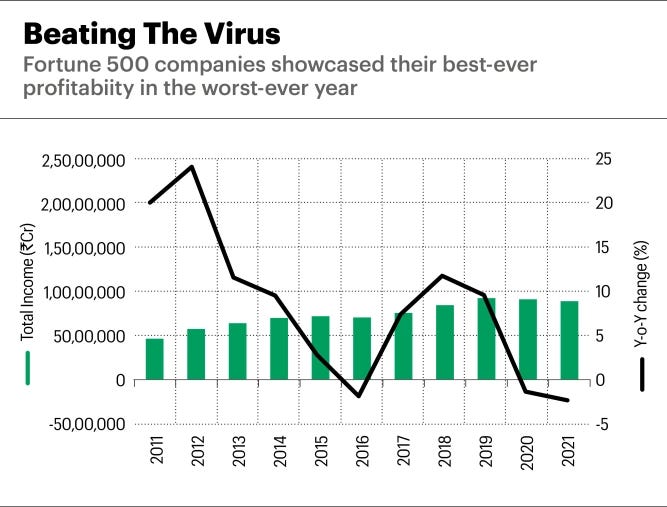

In 2021 corporate profit margins expanded dramatically. In FY21, the net profit of listed companies (more than 4,000) recorded a historic high, up 57.6%; what’s more interesting is that the overall Y-o-Y revenue slid 2.4%. That means the entire 57.6% rise in profits came from the expansion of profit margins.

Has the new era of technology-induced corporate efficiency descended upon us? Are we in a new economy, a higher profit margin paradigm? The answer to all questions is no.

As much as we would love to believe that productivity improvements brought to us by technological innovations will transform into corporate profitability, historically, that has not been the case. Every time such a broad-based profitability rise has occurred in any industry, sector, or economy, the ultimate beneficiaries are the consumers. The beauty of capitalism is that such high-profit margins will lead to new companies entering the market and undercutting the old prices, eventually making the profit margins revert to mean sooner.

Until now, the fall in the stock market has been due to P/E contraction because of rising interest rates. Once corporate profit margins start reverting to the mean, we can expect a more significant decline in the overall market. As to when we can expect profit margins to begin shrinking, I have no more insight into it than anybody else, but I am counting on it to happen sooner rather than later.