The Nifty 50 — A Deeper Look

Breaking down where the last decade’s returns came from, and what that might imply for the next one

It started with your neighbour.

Maybe it was 2020, maybe 2021. The world was locked down, offices were shut, and somehow, inexplicably, the stock market was going up. Your neighbour, the one who never seemed particularly financially savvy, was suddenly talking about his portfolio at every family gathering. His mutual funds had doubled. His Zerodha account was up 80%. He had opinions about IPOs.

You watched. And it stung, not because you wished him ill, but because you hadn’t done what he had. As the dialogue goes, “dost ke first aane ka dukh, uske fail hone se zyada hota hai.”

Charlie Munger put the same feeling in plainer terms: the world is driven by envy, not greed.

That envy brought crores of first-time investors into the market. And the infrastructure was perfectly ready for them. SIPs made it frictionless, ₹500 a month, auto-debit, done. And a decade of “Mutual Fund Sahi Hai” had already done the convincing. Investing in equity, once considered risky and speculative, had been rebranded as the obviously responsible, obviously correct thing to do. The ads said so. Your neighbour’s portfolio said so. Your Instagram feed said so.

Warren Buffett once observed that legitimate theories frequently lie at the root of financial excesses, good ideas simply carried too far. The idea that equity markets outperform over the long run is not wrong. It is well supported by evidence and history. But somewhere between that truth and ₹31,000 crore of monthly SIP inflows flowing almost entirely into large-cap Nifty 50 stocks, something shifted. A sound investment principle quietly became an unexamined reflex.

Almost nobody was buying equities at the market lows of 2009 and 2020. Today, almost everybody knows that stocks will outperform over the long run. That shift in consensus is worth pausing on.

So what exactly are these investors buying? When you put money into a large-cap fund, a flexi-cap fund, or even many mid and small-cap schemes, you are, one way or another, overwhelmingly buying the Nifty 50. Over 50% of flexi-cap holdings are Nifty 50 stocks. Even mid and small-cap schemes park close to 30% of their money in Nifty 50 names. The Nifty 50 is, for better or worse, the engine of the Indian retail investor’s wealth.

And most investors have never stopped to ask: at what price, and on what assumptions?

That is the question this piece tries to answer, not through charts, not through economic forecasting, and certainly not through witchcraft. But through a simple, rigorous framework that breaks down exactly where returns come from, where they came from over the last decade, and what that tells us about the decade ahead.

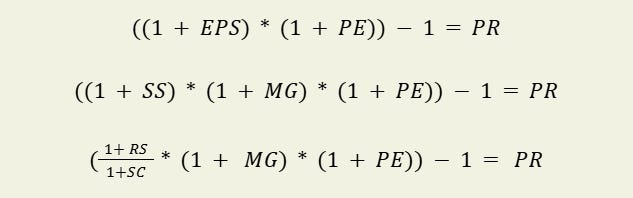

Five factors combine to determine total investment returns in common stocks:

• Rupee sales growth

• Changes in profit margins

• Changes in the multiple paid to earnings

• Changes in shares outstanding

• Dividend yields

The total return from common stocks, whether the entire market, an index or an individual stock, derives from five factors but begins by breaking return down into three base components – growth in earnings per share, change in the P/E multiple, and return from dividends.

Total return is easily calculated by multiplying the change in EPS by multiple growth and adding the dividend yield:

Total Return = (EPS Growth x Change in P/E Multiple) + Dividend Yield

Growth in earnings per share can be further derived from change in the net margin and change in sales per share:

EPS Growth = Sales Per Share Growth * Margin Growth

Sales per share growth can be further broken down into Sales Growth in Rupees divided by Change in number of shares outstanding:

Sales Per Share Growth = Sales Growth in ₹ / Change in Shares Outstanding

Calculation of annual price return (PR below or Price Return) broken down by the full set of variables (again, other than dividend yield) is a multiplicative function of each component. Formulaically, the amount of “1” is added to the percent growth rate for each component, with the amount of “1” then subtracted after the multiplicative function to arrive at a percent return.

And for Total Return (TR), we add the Dividend Yield (DY) to Price Return (PR):

For the above formulas, the variables are:

Growth Rates Approximate the proportion of return attributed to each factor but are not precisely mathematically correct. For the ease of math and use for those interested in utilizing the five factors I am content with the math roughly being right.

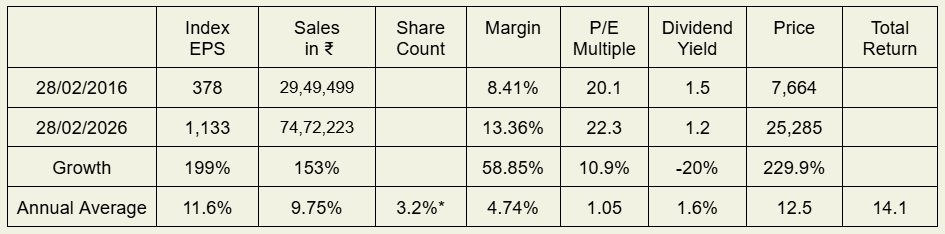

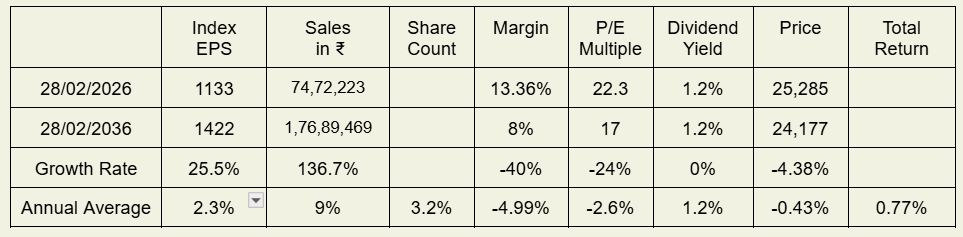

On the surface, the Nifty 50 looks reasonably priced. A P/E of 22.3 is neither cheap nor expensive, it sits almost exactly at its long-term median of 22.5. Glance at that number and it’s easy to conclude that the market is fairly valued, and that the next decade should look roughly like the last one.

Most retail investors are doing exactly that, extrapolating the last decade’s returns of close to 14-15% annually and expecting more of the same.

But the surface is precisely where you shouldn’t stop.

Look at the table again. Of the roughly 14% annual return the Nifty 50 delivered over the last decade, nearly 4.5% came from a single source, expanding profit margins. Strip that out and the index returned somewhere in the 7-8% range. That’s not a bad return, but it’s not the double-digit compounder your neighbour was bragging about at dinner. It’s closer to a government bond with more volatility.

The uncomfortable question is: can margins expand from here?

Almost certainly not at the same pace. Margins of 13.36% are close to a secular peak by any historical measure. Adam Smith’s invisible hand has a long memory, high returns in industries with low barriers to entry attract competition, and competition compresses margins.

The laws of economics can be ignored, but they cannot be repealed. What took a decade of favorable conditions to build can erode quietly and steadily.

So if margins can’t be counted on, perhaps growth picks up the slack?

That’s a harder case to make than it sounds. The Nifty 50’s strong revenue growth over the last decade was flattered by two things — a sharp post-Covid snapback and a prolonged period of elevated inflation, where rising input costs were simply passed through to the customer.

Both of those tailwinds are fading. It becomes genuinely difficult to build a credible case for sustained 10% revenue growth when nominal GDP is likely to expand closer to the mid-single digits.

The math is not complicated. It’s just uncomfortable.

The retail investor who came into the market watching their neighbour get rich, who was told by every ad and every influencer that equity is safe and SIPs are the answer, is working with an expectation shaped by an unusually favorable decade.

A decade where margins expanded, where post-Covid growth was extraordinary, where multiple factors aligned in the market’s favor simultaneously. Expecting that to simply repeat is not optimism. It’s extrapolation, and extrapolation is one of the most expensive habits in investing.

The Multiplicative dance of these factors is useful for assessing past returns. Their interplay is equally useful in helping project future returns.

Discounted-cash-flow analysis gets the investor to the same place but spending time analyzing the impacts on and sources of sales growth, how and why profit margins changed or may change is far more meaningful than debating terminal growth rate beginning a decade or more from now or considering beta as a component of measuring the cost of equity capital

The future direction and rate of change of the five factors is essential in the analysis and valuation of business. Spend too little time or no time thinking through the futures and well, good luck.

Today Nifty 50 investors are certainly entitled to their belief of 12-15% returns annually. But plug in any combination of expectations for the factors and see what you come up with.

I further don’t endorse the short-term buying and selling of the broad stock market based on technical analysis, economic forecasting or witchcraft. That’s market timing and I don’t know anybody that got rich practicing what in modern times is called day-trading.

I know plenty of both rich people that trade and poor people that trade, but the rich ones didn’t get rich that way. Some of the poor ones did get so that way, having formerly been rich.

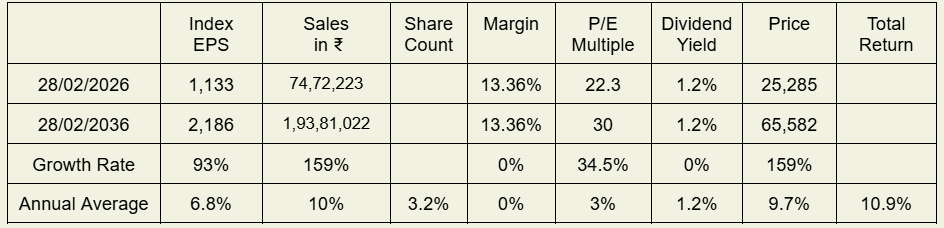

Bull Case

A Bullish scenario would likely be profit margins holding at an all time high of 13.36%.

Revenue keeps growing at a high rate of close to 10%. With business performing in such a way, a higher valuation multiple of close to 30 is much more likely.

Even in such a rosy and bullish scenario, returns seem to be lower than investors expectation of 12-15% annually.

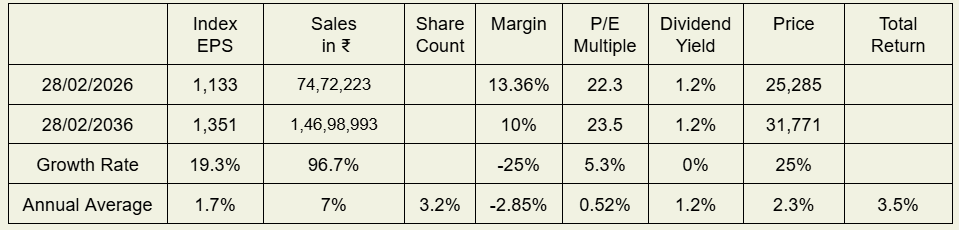

Base Case

With inflation settling down, sales are likely to grow at a lower rate, closer to the rate of GDP growth rather than close to double digit numbers. Margins declining from what seems like a secular peak to close to 10%, which is still a figure considered very high by historical standards.

A valuation multiple close to the long-term median is a good marker to set the base case.

Even in such a scenario we can likely expect much more sober returns.

Bear Case

Contemplate a more bearish scenario, higher Inflation returns due to global conflict.

Higher Inflation will likely lead to higher sales but lower profit margins.

The years 2021 to 2025 did see more rapid sales growth, courtesy of snap back from a revenue hit in 2020 but also due to high inflation, where higher cost of goods sold and labor expense were passed through to the customer.

P/E Multiples are likely to contract to close to 17 due rising interest rates in a high inflation environment.

If one simply averages these three scenarios, the implied return comes out to roughly 5% annually for the next decade. And with 10 year Govt Bond hovering around 7%, one should really question investing in a broad market index/ mutual fund.

None of this means investors should abandon equities or attempt to time the market. But it may be worth reconsidering the assumptions behind the effortless 12–15% return expectations that have quietly become the default.

The five-factor return decomposition framework used in this analysis was first introduced by Chris Bloomstran in the Semper Augustus Investments Group annual letter. If this framework resonated with you, the letters are worth every hour you spend reading them.

Excellent piece almost like dissertation! We need not agree on all points but can’t argue on most as well.

This article talks about certain things which are too exaggerated and conceptually flawed:

1. The Nifty long-term average returns are closer to the Nominal GDP growth of the country which is Real GDP growth + inflation.

2. Also, it assumes that the composition of Nifty will remain same over time and no new companies will enter the index.

3. The long-term median multiple of nifty is close to 21-22x so I am not able to grasp from where the valuation multiple of 30x came from.

4. Assumption that inflationary scenario will last over 10 years is a hyopthetical scenario. Generally interest cycle move between 4-5 years from peak to trough to peak.

5. Assumption if the stock market returns come down over time the government bond yield will remain at the current level of 7-8%. This I don't see happening unless there is severe structural problem in the Indian economy because even theoretically the equity returns are Risk free rate + Risk premium of equity.

In this scenario of 7-8% (which is higher than stock returns) people will just hoard money which will push RBI to cut down the interest rates and push consumption.

I only agree with the point that returns will come down, but it would be because of base effect as the Indian economy grows larger in size the rate of incremental growth will come down + the risk perception of the Indian economy will come down which will reduce the overall interest rates in economy and also the premium that investors demand from the Indian stock market.

Overall, this article points to the scenario which are too exaggerated or hypothetical. The scenarios presented here are the bet against the Indian economy in which case I will be least worried about equity investing.