Ujjivan Financial Services(BSE: 539874)

Ujjivan Financial Services(BSE: 539874)

A Rare Merger Arbitrage Opportunity

In India, most arbitrage funds take part in arbitraging futures against current indices, which do not produce good returns over long periods (3-4%). No pure merger arbitrage funds exist because of the myriad of current confusing rules.

Even after sending SEBI and the NSE emails asking for stuff to read on Merger Arb, I am still confused about the laws.

But every once in a while, even this confusing place can throw out a golden nugget for the ones still paying attention and trying to do the tedious task of sifting through the debris after everybody else has given up. Great Opportunities can always be found doing tedious things that no one else is willing to do.

Ujjivan financial services is one such opportunity right now.

Ujjivan financial services, which has a current market cap of Rs.1865 Cr, owns 83.3% of Ujjivan Financial Bank, which has a market cap of Rs.2791Cr. Even a basic sum of the part calculation shows that UFS should be worth at least Rs2324.9 Cr(83.3% of 2791), representing a 19% discount from its current Valuation.

In 2021 RBI allowed holding companies to reverse merge with corresponding banks after five years of operations. UFB started in 2017; therefore, the five-year window has already passed. The boards of both the companies have already agreed to the reverse merger.

Under the reverse merger agreement, every share of UFS will be exchanged for 11.5 shares of UFB.

CASE 1 [BASE CASE]:

Assumption: The return on the transaction stays the same as today.

Cost of 1 share of UFS= Rs152.80

Value of 11.5 shares of UFB= Rs185.70(16.15 x 11.5)

Total return = 21.5%

Expected Closing = 1st May 2023 (294 days)

Annualized Return = 26.75%

CASE 2 [BEAR CASE]:

Assumption: UFB share price falls to book value(Rs.14.81), and the merger takes longer than expected.

Cost of 1 share of UFS= Rs152.80

Value of 11.5 shares of UFB= Rs170.31(14.81 x 11.5)

Total return = 11.46%

Expected Closing = 1st August 2023 (386 days)

Annualized Return = 10.83%

CASE 3 [BULL CASE] (Most likely to happen):

Assumption: Banking performance recovers and improves UFBs valuation.

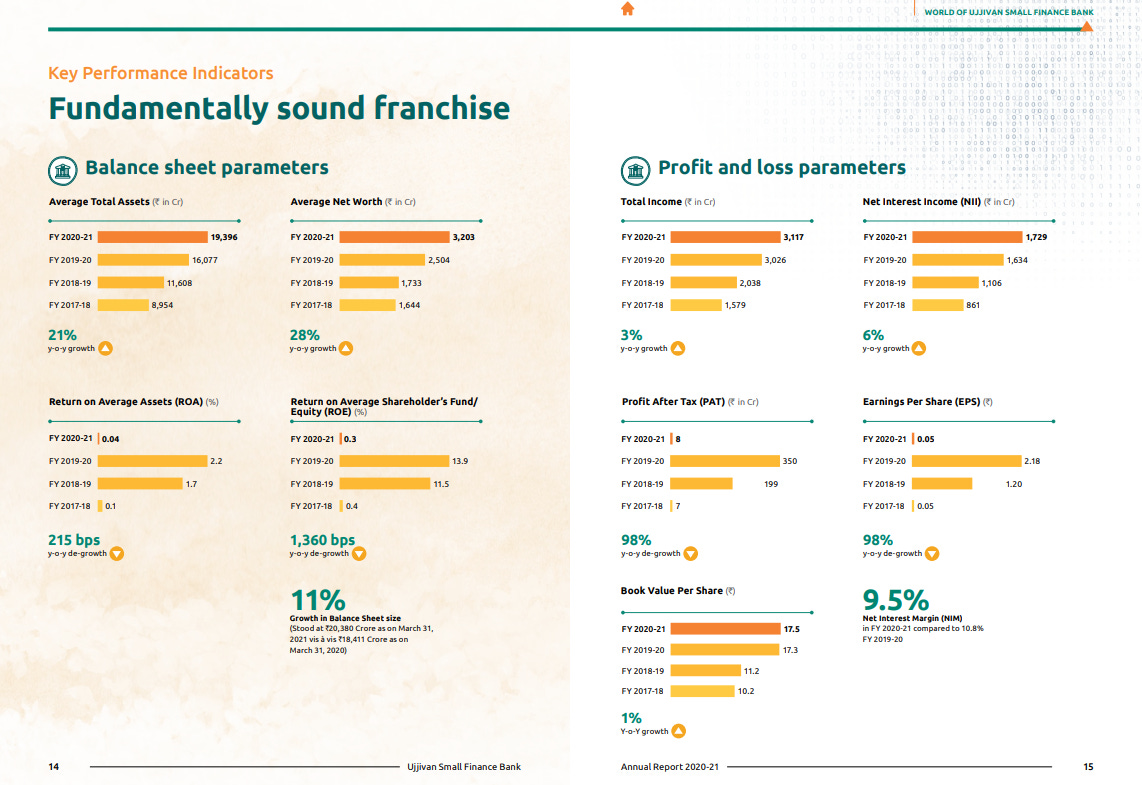

A little history of the bank

Total assets more than doubled from FY 17-18 to FY 20-21. The loan book has doubled and is supported by deposits which have grown three times. Disbursements grew well till covid. Current and Savings Account (CASA) has gone up 20x in the last three years. CASA is a cheaper form of deposit which has helped the bank keep costs low.

Total income and net income have doubled. Profit after tax(PAT) and Earnings Per Share(EPS) were heavily impacted by COVID-19 but had grown significantly before that.

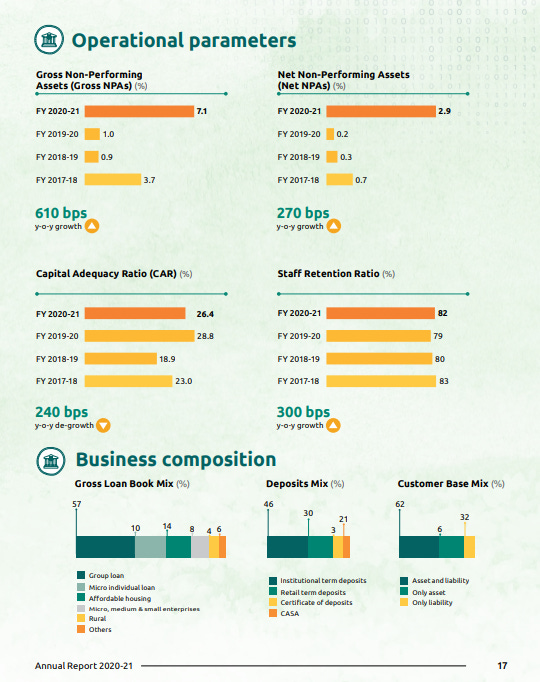

Gross Non-performing Assets and Net Non-performing Assets jumped significantly in FY20-21, but the bank remains well-capitalized.

Current Performance of the bank and why banking performance recovery is the most likely scenario:

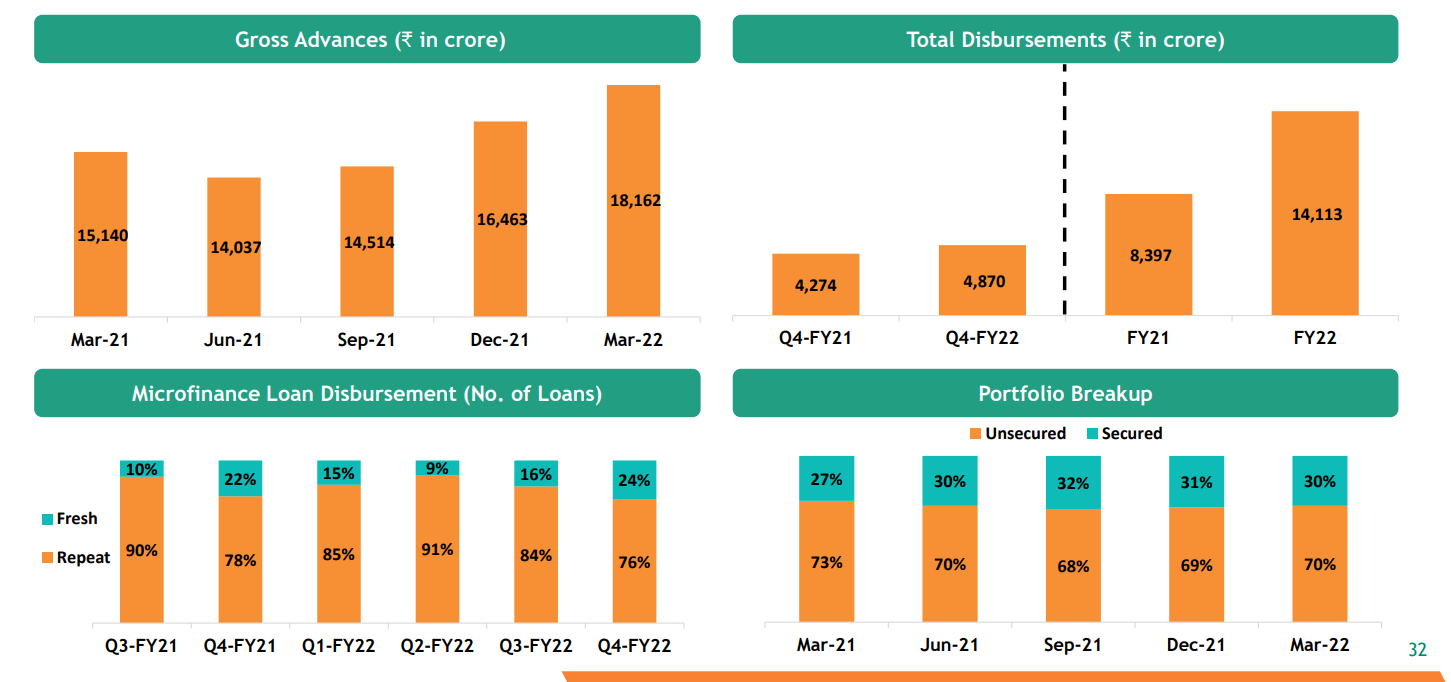

Highest ever quarterly disbursements in a row; ₹ 4,870 Cr up 14.0% Y-o-Y; up 1.3% Q-o-Q

The growth in disbursements has come in the most recent quarters, and most of the disbursements have gone to its existing customers.

Also, the bank is slowly but steadily moving towards more of its loan book secured, showing an asset quality improvement.

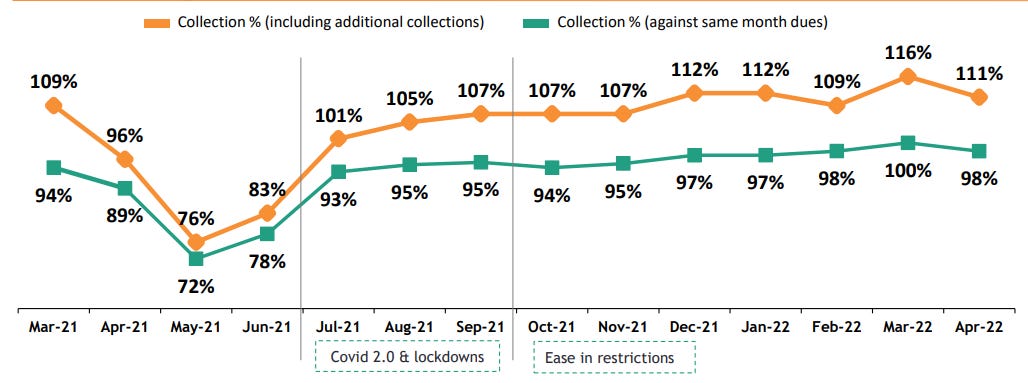

Collection efficiency at ~100% in Mar ’22

Collections have picked up significantly over the past ten months, leading to better asset quality in the future.

As you can see from the graph above, same-month collections are close to 100%, which means the bank is also collecting arrears built up due to covid.

Arrear collection has been steadily increasing since Jun ’21. All the past dues collected by the bank is the primary reason the bank’s performance is expected to improve. It will also lead to the bank reversing some of the provisions it had created due to covid.

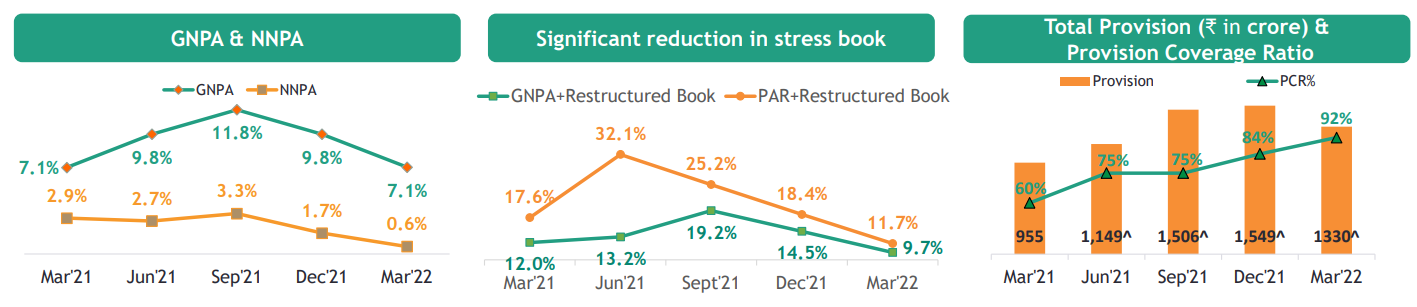

Improvement in GNPA and NNPA

The bank was hit very hard due to covid since it lends to the lowest segment of society.

GNPA, which peaked at 11.8% in Sep ’21, is declining at a healthy rate and has come down to 7.1%.

NNPA has come down from 2.9% to 0.6% because of the aggressive provisions taken by the bank, which do not include the write-offs the bank has taken

The aggressive provisions have led to the bank’s superior Provision Coverage Ratio of 92%.

Profitability

The bank returned to profitability in Q4 after taking some significant losses in Q1 & Q2 due to the second wave of covid-19.

The profitability will likely rise in the coming quarters due to reduced collection costs, lowering GNPA & NNPA, and reduced provisions.

Additional Catalyst

In India, a bank can apply for a universal banking license after five years of operations, and as we have already stated, the five-year period has already lapsed.

A universal banking license will free UFB from many additional requirements that a small finance bank must adhere to.

VALUATION

Looking at similar banks in the market, UFB is expected to trade at around two times the book value.

Expected Market Price of UFB = Rs 30(15x2)

Cost of 1 share of UFS= Rs152.80

Value of 11.5 shares of UFB= Rs345(30 x 11.5)

Total return = 125.7%

Expected Closing = January 11, 2024 (A more extended period has been taken for UFB to realize its value)

Annualized Return = 83.62%

Disclaimer: I currently do not hold a position in UFS or UFB but plan to build one after this article is published.